Special Reports + Analysis

Let’s Talk Industrial

Sixteen distinct markets help define industrial inkjet printing.

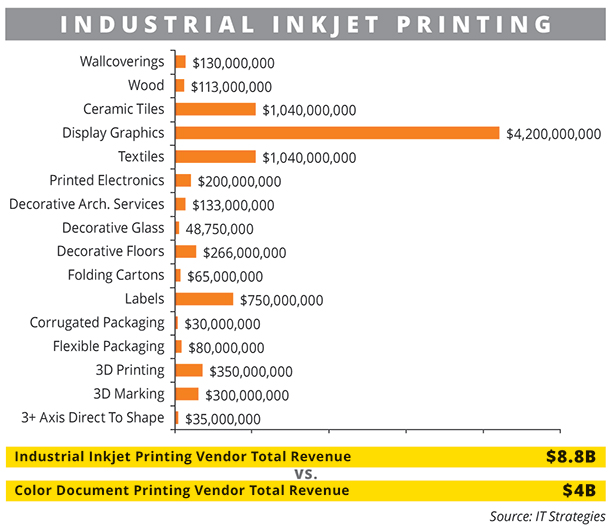

The term “industrial printing” can be confusing because it’s defined in so many ways. At IT Strategies, we define it as all digital print that takes place outside the office. When you look in more detail at the evolution of these non-office markets, you see that many of them are in fact some derivation of technology first deployed in wide-format graphics. That’s not surprising when you see that the wide-format market was, and has remained, the largest single revenue source for non-office digital print by a fair margin (see chart below). Wide format has been both a generator of investment dollars and a technology platform, in much the same way that high-volume document color printing has been driven by electrophotographic digital presses.

As you’ll see in the chart, industrial digital markets as we define them are broken down into 16 distinct segments. It’s significant, and a good sign for the future, that over the last 20 years, these 16 separate, real markets for digital industrial/production print technology have opened. Most are at an early stage of development and are based on high-value, low-volume models (relative to analog print). For the technology developers, it’s almost never a simple replacement of analog print technology (though there has been one interesting exception in the ceramic tile industry); this is probably good, because the technology and economic evolution path is necessarily slow and complex.

Multiple-Axis Direct to Shape

Multiple-Axis Direct to Shape

This market has accelerated significantly in the last two years. It started with a couple of bottle printing systems (KHS and Krones) and now includes more than 20 products that mostly target cylindrical packaging like cans, but also true 3D systems like Heidelberg’s Omnifire and Xerox’s direct-to-object inkjet printer. They enable very short run printing of promotional items and early customized manufactured products like car interiors (on the Omnifire). It’s exciting, but highly specialized, technology. The sector has not yet progressed to a production scale, with systems priced around $100,000 to $200,000 and some coming in at $500,000-plus. Some have argued that direct print should replace labels in the name of lower costs and less waste, but the debate is ongoing.

3D Marking and Promotional Goods Printing

3D Marking and Promotional Goods Printing

Over the last three to five years, the market for flatbed UV inkjet systems under $30,000 has developed to a quarter of a billion dollars in vendor revenue. These systems feature deep platens that are able to accept basically flat manufactured products (think iPhone covers) in a variety of thicknesses; they can print a little over beveled edges, too. This has proved a popular market for Mimaki, Roland, Mutoh, and others, and it addresses the very lucrative promotional goods industry. The real long-term target, however, is the ability to decorate virtually all manufactured products in some way or another. Today, that market is split by verticals and is mostly served by semicaptive product decorators as well as local screen/pad printers and in-house decoration shops. The argument for inkjet is strong, since pad and screen are essentially manual batch print techniques unable to vary images or apply really sophisticated color.

3D Printing

3D Printing

3D inkjet printing has become more mainstream in the last three to four years, with most of the emphasis going to powder-bed systems that are often used to make custom molds, as well as some activity with functional UV-curable materials deposited by drop-on-demand inkjet. HP, with its Multi Jet Fusion technology, is betting a lot on industrial-scale powder-bed systems for true mid-level production competitive with and much more flexible than vacuum forming. There’s every reason to expect this to take 3D inkjet printing to a new level given the investments HP has made, lending more and more credibility to inkjet as a valid manufacturing process.

Advertisement Flexible Packaging

Flexible Packaging

Many inkjet developers are keenly eyeing packaging as a growth opportunity. Flexible packaging is easily the leading sector in terms of value and innovation, if not growth and volume as well; this industry is unusually aware of digital printing’s potential to address fragmenting consumer groups more efficiently with much shorter runs, as well as to tie print into the live data stream, including social media. There’s been small but important early progress using liquid toner in HP Indigo systems, as well as multiple aqueous inkjet projects designed to meet the consumer packaged goods’ preference for water-based inks. But the flexible packaging market uses large amounts of film; solving the riddle of how to print that at high speeds with inkjet is not going to be simple. But this industry is ready to experiment.

Corrugated Packaging

Corrugated Packaging

Most of the digital print action in packaging that we’ve heard about over the last year since drupa has been around corrugated applications. This industry is almost entirely analog today and sees great potential in inkjet. Preprinting the liners before (and in line with) the corrugation process could cut significant costs, and moving the decoration of blank corrugated sheets to be closer and more relevant to the user would bring additional advantages. The pace at which aqueous and UV inkjet systems are being brought to market (by such major suppliers as EFI, HP, KBA, Durst, Inca, and others) can only be called impressive. Part of the background to this growth is that the use of corrugated packaging at the retail level has expanded, so that the needs for higher quality color within this huge market (2700 billion square feet of output per year) are increasing. Drivers include the use of secondary packaging in primary retail locations, e-commerce, and expanding markets for heavy consumer goods and associated display materials. This market will act as a driver like no other in the development of faster, more reliable, more economical, and higher quality inkjet production presses with benefits that can then be brought to other sectors faster than would otherwise be the case.

Labels

Labels

Production digital printing of labels has been happening for more than 20 years, and now represents about five percent of output, 15 percent of revenues, and probably a much larger share of profits. This market shows digital’s ability to enter and live alongside an old-line analog technology, but it also shows how digital often lives off lower quantities and higher margins. Those higher margins are what users who have embraced digital are most fond of. At the same time, there’s a strong dynamic among the leading converters for much higher productivity from digital, and that’s driving interest in new hybrid lines that combine digital and analog printing, in addition to the general demand for higher throughput.

Folding Carton

Folding Carton

The offset-printed folding carton is a target for vendors of B2-plus digital sheet-fed presses like HP Indigo, Fujifilm, Konica Minolta, and Landa, among others. Digital technology has not yet made a big dent, though a lot of test marketing is undertaken on A3-format electrophotographic printers from vendors like Xerox. The analog folding carton market is much like commercial offset printing: commoditized and perhaps oversupplied. Folding carton itself has also steadily lost share among packaging formats. Still, it’s a large industry and there are valuable sub-sectors at the top of the market including cosmetics, beauty, and high-priced food and drink, so the issue is not lack of opportunity so much as a scarcity of suitable presses. A further difficulty for vendors is sorting through the vast number of commercial printers and folding carton converters to find ones with the capability and desire to develop new markets. This industry does not embrace digital as readily as others, like flexible packaging.

Decorative Floors

Decorative Floors

Floors technically include ceramic tiles, carpets, wood, and laminates, though these are often viewed as separate markets in their own right. That makes it hard to agree on what the core market is. Carpets are digitally printed to a modest extent and, of course, almost all ceramic tiles are digitally printed today. There is also a small, specialized market for printing wood for some flooring applications. Finally, new vinyl flooring types have emerged that reassert themselves up the value chain as high-quality products, and they are beginning to be digitally printed, though not always with dedicated systems. On top of all that market complexity, there’s an embedded perception among consumers dating from the predigital days that print on floors is a low-end product for those who didn’t want to spend money on real wood or stone. So, digitally printed flooring exists in more than one form, each specialized and relatively small in volume today. A single, dominant digital flooring dynamic hasn’t emerged as of yet.

Decorative Glass

Decorative Glass

Flat glass is a truly specialized substrate. The principal point of flat glass is often its transparency, though glass does get treated in different ways as a means of controlling ambient environments. Many of these treatments are applied during manufacturing and are not printing or patterning processes, though there are exceptions, such as automotive and some architectural glass. An Israeli company called Dip-Tech specializes in producing very large flatbed inkjet systems using frit inks (ceramic pigments that become permanently part of the glass on firing). These are built in particular to be able to handle the enormous weight of glass panels. Some printing of glass surfaces is done with UV ink on flatbed systems; other decoration is done indirectly with static film that is digitally printed and then applied later. This is truly a specialist’s market.

Advertisement Decorative Architectural Surfaces

Decorative Architectural Surfaces

Usually, this term refers to laminate substrates, which are essentially multiple layers of paper and sometimes other substrates permeated with resin and formed into a solid material under high heat and pressure. Print is often applied to a final paper surface under the last clear resin overlay of the substrate. There have been attempts to bring digital print to this market for 20 years; to date, only about half of one percent of this small market (97 to 108 billion square feet, globally) is digital. Flatbed UV and aqueous systems are the most common digital technologies for laminates, not always purpose built as you might expect. While developers have made cogent arguments over the years on why the laminate industry should adopt digital printing – the demand for customized, lifestyle-type environments (think fields of flowers on surfaces in a hospital) – the strategic potential isn’t connecting for reasons that are not fully clear. Perhaps the traditionally low perceived value of laminates in the minds of buyers is a barrier.

Printed Electronics

Printed Electronics

In the electronics industry, components are made by batch manufacturing processes. For example, LCD panels are made on single, super-large glass substrates that are then cut down to consumer size in an automated process. Semiconductors are made this way, as well. The dream is to come up with a roll-to-roll manufacturing technique for functional components, which has created interest over the years in using the patterning and chemical-application techniques of the print industry (certainly not just digital print, by the way). But beyond the already established and relatively crude screen printing of circuit boards, the use of print to manufacture these components has not really taken off. This has to do with the paucity of room temperature chemistries (necessary for print processes as we know them) with the appropriate functionality (like speed of charge transmission, for example) as much as anything. The drive toward ever smaller components is another obstacle, as there are limits in taking any form of print from macro- to nano-scale. Some work continues to bring inkjet into these fields, but true electronics patterning is still at an early stage. By the way, the printing of electronic patterns should not be confused with the coating of active chemistries such as photoluminescents or organic photovoltaics, applications where screen printing is widely used.

Textiles

Textiles

Textiles are a huge success story for digital print. The victory has been two-fold – at the low end with dye sublimation for both fashion and soft signage, and at the high end with reactive dyes for production roll-to-roll printing. The excellent functionality of textiles as a light, easily transported, and brilliant form of signage has been one key market driver. But even more important, digital printing answers key demands in the apparel world at both the high and low end of the market. The fashion industry is driven by very fast cycles, with social media and fragmentation of markets placing a huge premium on short runs, fast supply, and rapid change. These are core benefits of digital print (though digital is not facing a static competitor in screen print). This market is getting close to a steep commercial development curve, though it’s also dependent on major changes in brand- and retail-driven supply chains that are out of the technology developers’ control.

Display Graphics

Display Graphics

Display graphics is a 20-plus-year-old market. From a vendor perspective, it feels very mature as a by-product of the brutal competition in this sector. But despite falling hardware and ink prices, the market is still growing healthily in terms of demand. Wide-format inkjet comprises many applications, but the core driver remains the ability to provide local retailers with P-O-P graphics, supporting the sale of consumer goods and serving a function that can be called strategic to the consumer economy. The value of printed and converted output from this industry globally is more than $40 billion. Wide format has also given rise to technologies that have been applied in other markets such as direct to shape and textile. Those new applications represent a further 30 percent of value beyond the original wide-format market.

Ceramic Tiles

Ceramic Tiles

We like to say that the rule of production in digital markets is that they coexist alongside analog print doing different things and often not affecting the existing technologies directly. (Wide format is a great example.) However, the ceramic tile industry is the exception to that theory. The previous print process used for ceramic tiles was clumsy, slow, very expensive, and inconsistent; changes in the print results dissatisfied buyers and could even cause manufacturing problems in firing the finished tiles. It’s also exceptional that most of the work to develop printers that could jet ceramic pigments (theoretically a difficult chemistry for inkjet) was undertaken by the existing analog vendors and not the true digital print community. The result is that we’re approaching 80 percent market penetration, nearly a complete technology substitution by digital, after only 12 years or so.

Wood

Wood

Wood is a very specialized market and can take many applied forms, but the two important sectors are flooring and doors. It’s not a large industry (with output well under 11 billion square feet and a market for fewer than 100 flatbed printers) and has been served well with digital print, particularly by a Spanish company called Barberan.

Advertisement Wallcoverings

Wallcoverings

In most of the world, wallcoverings are a good example of an established and conservative market. In fact, wallcovering usage varies greatly around the world based on strong cultural factors. This is another market where wholehearted efforts have been made for years to get digital printing into the mainstream supply chain. Digitally printed wallcoverings are quite popular today, and their usage is growing. This is another specialized market, but a much larger one with considerable consumer potential. Digital printing’s success – due in no small measure to the availability of a waterproof and odorless chemistry in HP’s latex technology – has occurred through the development of a separate, parallel retail and converter channel not within the traditional wallcoverings supply chain. Another driver was the emergence of wall graphics using removable adhesive and cut shapes to further leverage digital’s ability to print small quantities in varying forms.

Last Word

So, there you have it: industrial inkjet printing broken down into 16 categories. Sixteen different digital print markets that you can sink your teeth into. Will you stick to the tried-and-true display graphics sector, or is time to branch out and start printing on wood and ceramics, invest in 3D printing, or make a move to package printing? The ever-growing possibilities with digital print are truly endless – what will you print next?

Printvinyl Scored Print Media

New Printvinyl Scored wide-format print media features an easy-to-remove scored liner for creating decals, product stickers, packaging labels, and more. The precision-scored liner, with a 1.25” spacing on a 60” roll, guarantees a seamless and hassle-free removal process.

Konica Minolta Appoints Frank Mallozzi to President, IPP

This Wide-Format Pro Started at Age 11, and 32 Years Later, Still Loves What He’s Doing

Wide-Format Printers Share Their Thoughts on Business-Advice Books

This Wide-Format Pro Started at Age 11, and 32 Years Later, Still Loves What He’s Doing

Wide-Format Printers Share Their Thoughts on Business-Advice Books

Canon Designs Recognized With Internationally Renowned iF Design Awards for the 30th Consecutive Year

Bulletins

Get the most important news and business ideas from Big Picture magazine's news bulletin.

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoHere Are the Winners of the 2024 Best of Wide Format Awards

-

Columns2 months ago

Columns2 months agoHow Apps and Instruments Are Making Color Mobile

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoGraphics Turn an Eyesore Cooler Into a Showpiece Promo in Historic Plaza

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoColorado Town Hypes Its Incredible Natural Gifts in City Hall Rotunda Project

-

Blue Print2 weeks ago

Blue Print2 weeks agoThis Wide-Format Pro Started at Age 11, and 32 Years Later, Still Loves What He’s Doing

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoPrivate Customer’s Bespoke Bathroom Wallcovering Showcases Their Passions

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoIllinois Print Pros Help Historic Toy Brand Create a Memorable Shopping Environment

-

Best of Wide Format2 months ago

Best of Wide Format2 months agoIconic Music Venue Celebrates Half-Century With Vibrant Exhibit of Rock Artifacts